Make Europe Great Again

PIVOT OR DEATH! Future of the Euro. Trading the Bounce.

“Within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough.”

—Mario Draghi, 2012

"There is a risk our Europe could die. We are not equipped to face the risks.”

—Emanuel Macron, 2024

My work on Europe etc.

First Exit? ✍️

Reading Time: 16 minutes.

I expand on my thoughts on Europe’s decline, what I see as requirements to halt the decline, how I see the future unfolding and how I plan to play it. 3,500 words.

The EUR/USD is at 1.03 and awfully close to parity once again. Europe’s short-term solutions were proven to be just that — short term.

The problems Europe faces are complex and multi-layered, and in this piece we will attempt at isolating them one by one, looking into how they relate to each other and discuss potential scenaria for solutions and how this could play out.

We will continue where we left off, starting from post-Ukraine invasion times where things blew up — mostly in Europe’s face.

Where are we now?

Europe today is like a ship without a captain. We know this because the ship is sailing to nowhere and there is no captain (i.e. political leader) to change its course.

Macron has taken stabs at proclaiming grand ideals and a change of course, but that was probably an attempt to reset his chances of being re-elected while those ideals did not gain enough momentum to make a difference.

This is probably because in one part, those kinds of political speeches are labelled as alarmist and in the other part everyone knows the EU is dying but they are too focused on their own countries to do something about it.

Could that be another EU structural flaw? That the de facto leader of Europe could have conflicts of interest with Europe itself?

The President of the US technically has one country to run, while a political leader in the EU has his own country to run plus politics at the European level.

At the same time, the President of the European Commission is a European national (German, currently), is not voted by the European people but by MEPs — and is mainly focused in spreading her own agenda across Europe while paving the way for future personal arrangements to accommodate herself after she has left the Presidency… Future of the EU be damned!

Granted, politics isn’t perfect in the US or anywhere else for that matter — but the EU is on another level of imperfection.

European politics are further complicated by US involvement in European affairs, mostly to promote their own interests and keep the trading bloc on a leash lest it veers off course and causes problems to American global hegemony.

Yeah, I said it.

The Americans seem to not care that the EU is going through a serious existential crisis with possibly terminal outcomes, at all.

But Europe, if you don’t care for your own self, why do you expect others to care for you?

Europa is losing competitiveness, morale, prestige and her position on the global stage. The Americans need her to guard their interests while the Eastern bloc needs her to promote their own.

The Europeans themselves deep down still believe that they are peak civilisation and that they deserve everything while they still “bank” on the same things they had a century ago.

The results of all this is increased social and political turmoil, changes beneath and above the surface across the Union and a political-ruling class unable not only to keep up with the goings but to rule its people at a basic level.

The results of all this are obvious.

Europe’s challenges span both tangible and intangible — in the former, serious economic and structural issues and in the latter, more abstract cultural, social, political and moral dynamics that albeit result in tangible problems.

The Eurozone economy faces sluggish growth, persistent inflation, and uneven development across member states. The European Central Bank (ECB) finds itself constrained and limited, unable to address the diverse economic realities of its members with a one-size-fits-all monetary policy. Besides, this was one of the EU’s flaws from the outset.

Politically, the EU is increasingly divided. This plays out on the global stage where Europe’s influence is practically inexistent — stuck between the West and the East.

The EU’s inability to project a united front has diminished its influence on the global stage.

Culturally, the sense of a shared “European dream” has faded. Many citizens see EU institutions as out-of-touch bureaucracies that impose regulations without understanding local needs.

Let’s dive in…

When “Whatever It Takes” was not enough

Mario Draghi was deified for his famous speech that “Saved the Euro” in 2012 — but in economics (and especially central banking!) for every thing that is seen there is something that is unseen.

Obviously, markets and people will only see the short-term results while they’ll have to wait around to see the rest! In effect, what Draghi did was kick the can down the road of the EU’s reckless fiscal policies, allowed member-states to spend irresponsibly and stack up more sovereign debt — compounding the problem in the process.

I remember some 20 years ago, when the Euro and the EU was still on the up and up — the narrative was gaining ground that the Euro would outshine the Dollar and that it would become the next reserve currency.

After the European Debt Crisis of 2012 and beyond, the Europeans further pushed the button of bailouts, stimulus and even reforms to keep the Union’s fabric in one piece — but we mostly find ourselves in the same place some 15 years later.

Why?

Brussels, Regulation and the Business Environment.

We agree that the dynamics of business and competition are what drives an economy, right? And so without a vibrant private sector then we don’t have an economy.

Brussels (“the EU”) with its overly strict and top-down regulations and policies that are full of conflicts of interest and excess complexity have managed to kill business dynamism within the EU.

Members surrender sovereignty to the Union when they enter it with the notion that together we would all be better off. Well, it seems that designs on paper are seldom made the same in reality.

In fact, instead of everyone working together for a better collective future, blurred segregation lines started to be drawn where each single member pursued their own interests to the detriment of others.

One would say that this makes sense, countries do compete with each other on the global stage. Yes, but the European idea was built on the foundations of trust and cooperation. When countries start backstabbing each other, then we would all be worse off, the game becomes a minus-sum game.

Basically, domestic politics take precedent over EU politics — and it becomes one big mess. Take the example of energy security which blew up completely after the Russian invasion into Ukraine.

Each country had different relations as well as energy dependencies vis-á-vis Russia — applying a top down solution to that was never going to be optimal. The EU came out with a plan to “Repower the EU” but it was without long-term substance. THREAD.

It’s now obvious that Europe is losing competitiveness because it can’t procure energy competitively enough.

And this saga will be ongoing, especially after a certain someone decide to blow up the Nord Stream pipelines that transported gas from Russia to Germany…

Convenient, no?

The Financial Layer

Weak banks beget a weak economy, and a weak economy begets weak banks.

The GFC of 2008 left the broader banking system permanently scarred (some countries more than others), the EU was forced to create mechanisms to guard not only national banking systems but entire nations!

But Europe (i.e. Germany) dragged its feet for too long before it started to move, and only did so when it realised that “no man is an island”. By that time the intangible layers of trust and confidence had already been considerably eroded…

The Greek banking system was re-capitalised three times, and Cyprus infamously had to undergo through a deposit haircut to “recapitalise” its banking system. Meanwhile, Spain was luckier as it entered an assistance packaged with the ESM.

This lingering lack of trust coupled with no real measures from a united Europe to stimulate the economy resulted in a weak post-GFC rebound — which in turn resulted in weak capital markets. 🔄

The weak performance of investment fund managers post-2008 and the over-performance of the US versus Europe strengthened the hand of passive investing. More capital started to flow out of Europe and into the US, benefiting the US in a cyclical way. 🔄

Europe was left to deal with lagging stock market valuations, weakening competitive positions and an excessive regulatory environment which makes everything harder and less predictable. Super antibusiness.

Techno-Colonialism

European countries may have been the best in the game of typical colonialism, but they suck at techno-colonialism!

America’s pro-risk and future-oriented business culture, common language across the country and largely uniform laws meant it was easier to build tech and expand it across state borders without much friction.

On the contrary, Europe is exactly the opposite: Europe’s investment culture is too traditional and slow, with not much appetite for risk on projects like early-day Facebook and Google.

The gap is clear by now and this is why talent flees Europe for the US. Having political leaders announce incentive schemes to bring them and their tech companies back won’t do anything.

In fact, even if a European founder wants to build something from the ground up he will probably move out of Europe and go somewhere else. The regulate-to-death mentality of Europe and extreme costs to launch and run a business make it practically impossible.

All this vicious cycle creates un-alterable realities that self-reinforce it: The practical inexistence of tech in the EU means there aren’t any big VC funds strong enough to cut big deals with companies in the pre-IPO stage.

This is why even if a European company makes it big (e.g. Spotify), it moves to the US because that’s where the money and the best capital markets are — Europe is slowly becoming obsolete.

Fiscal Sanity and Realism

But even with all these problems and the fact that we are getting poorer (refer to the graphic below👇) with the passing of time, we still believe we should have everything.

We are still banking on success from half a century ago!

European self-entitlement acts like that, European nations act like that too! More context on European debt problems here.

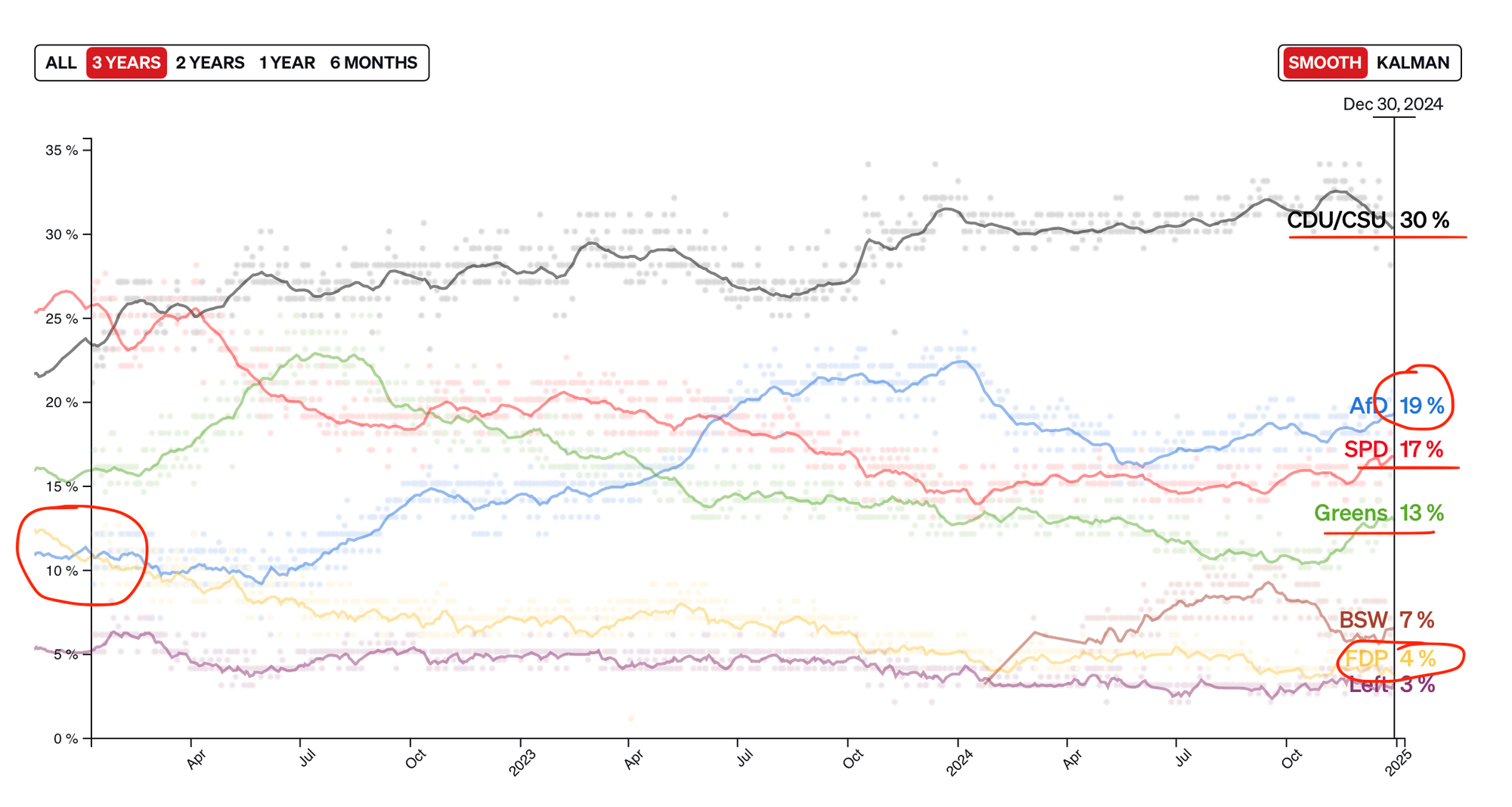

One of the few fiscally sane countries in Europe has also started to throw in the towel under the auspices of the traffic light coalition in Germany. In fact, the coalition failed early November 2024 when the Finance Minister wasn’t willing to “suspend” the debt brake under the requests of Scholz.

Note that former Finance Minister Lindner comes from the FDP (Junior partner in the coalition) while Scholz is from the SPD. The FDP has been tanking in the polls since it joined this coalition — which was one of the reasons I predicted they would eject themselves at some point.

—> Tweets on “FDP” from philoinvestor on X.

Chancellor Scholz wanted to suspend the debt brake to throw money from the treasury into the economy and create an illusion of prosperity, he argued that the debt brake wasn’t needed because German Debt/GDP is much better than the French or the Italian one.

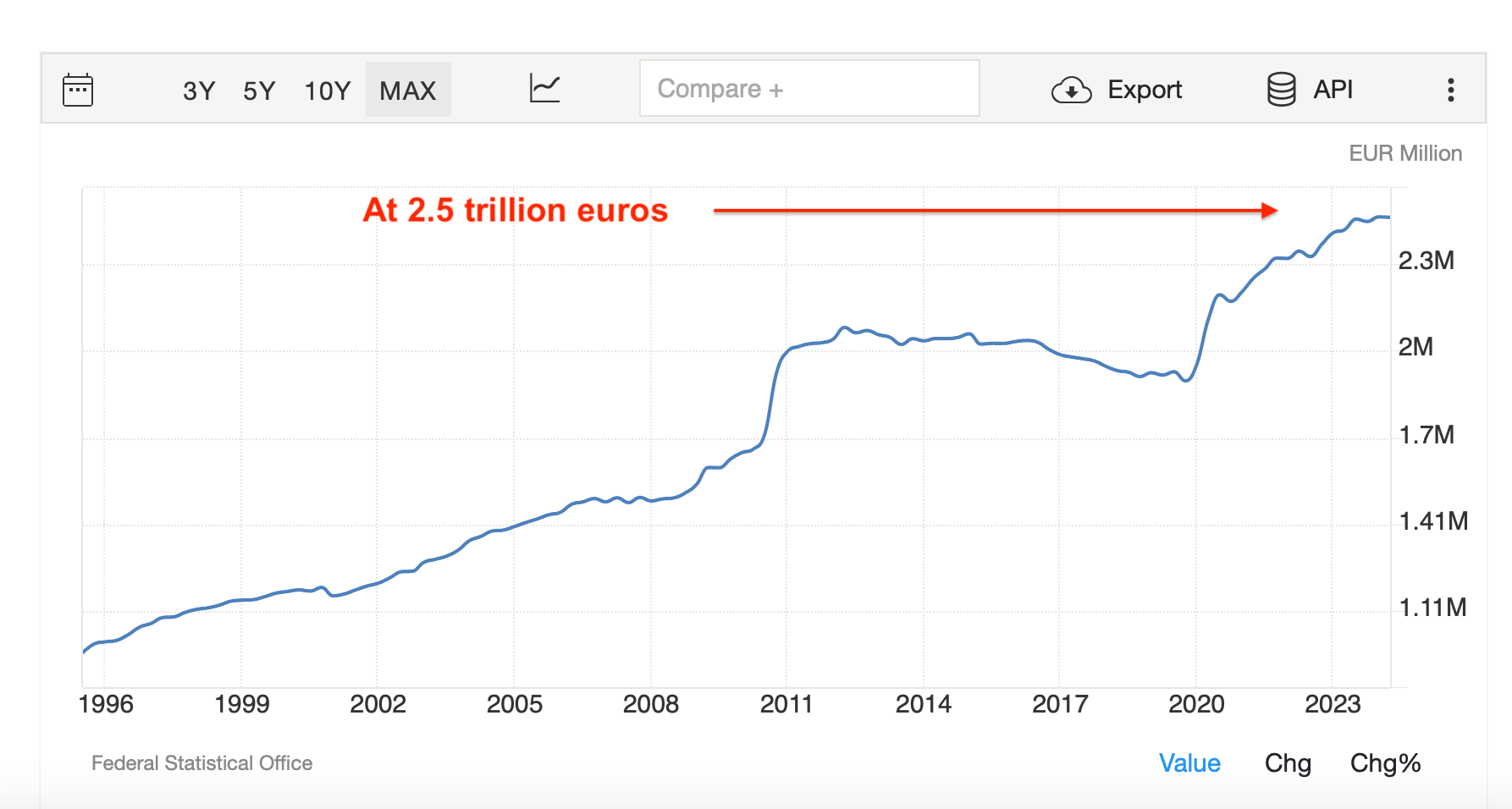

Well, obviously Olaf. But how long can that go? When you have a look at German Debt/GDP you get the idea that all is well in Deutschland… But that’s only because the denominator (the GDP) has been increased by high inflation while the Debt hasn’t gone up by that much.

Great way to stay debt sustainable right? 🥲

When you scratch the surface you see that the German economy has been going sideways since 2019 while the absolute levels of debt have been going up and up.

Real GDP is the same since 2019, it’s inflation that increased it — making Debt/GDP % look just fine. All this while Debt has actually been going up just fine 👇

Government debt trajectories differ by member state but the Eurozone average picture is clear — increasing government debt while productivity is going down.

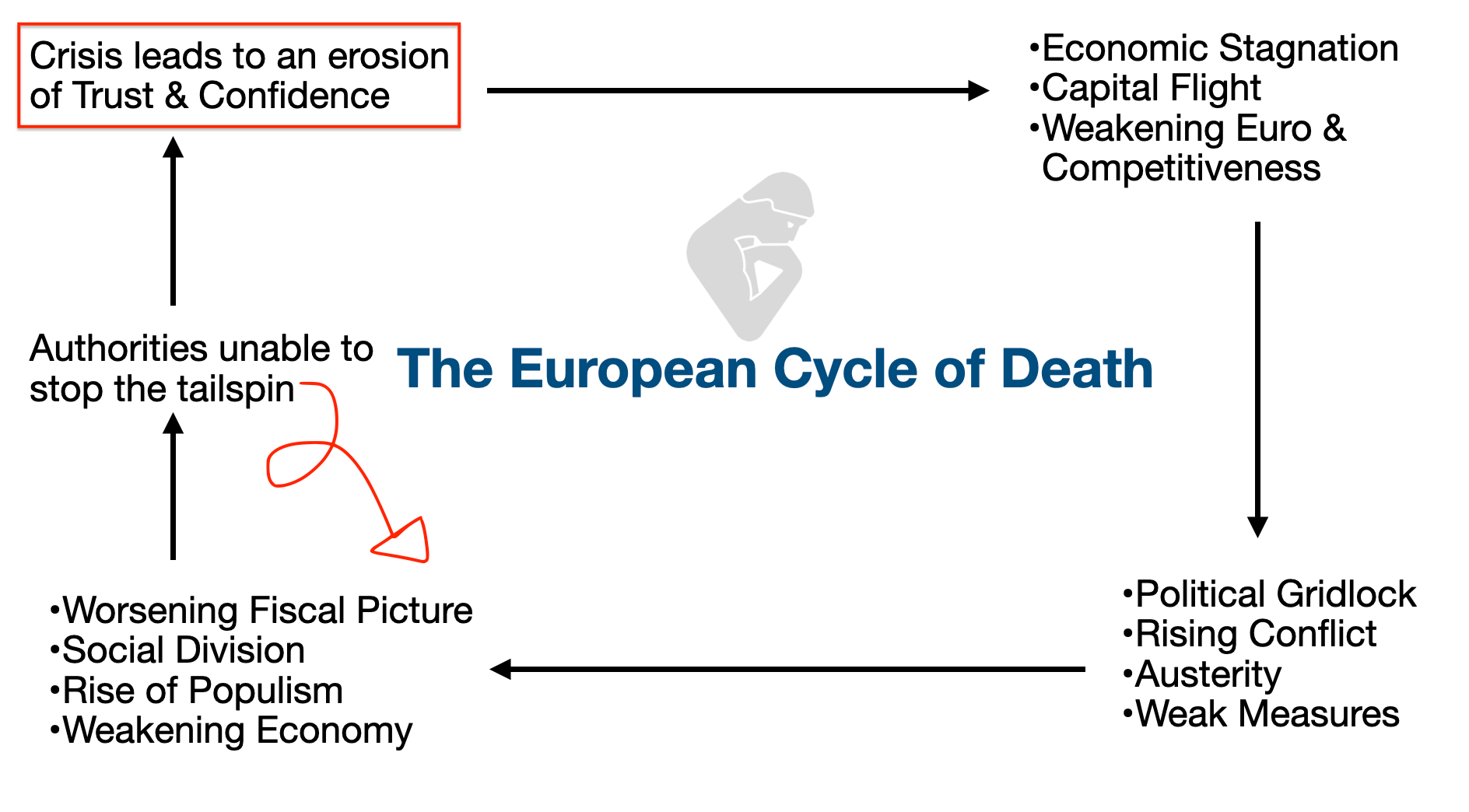

All these layers working together create further distrust in EU institutions, reinforcing the vicious cycle and the “negative bubble” that the EU finds itself in.

So what needs to be done for Europe to have a fighting chance? How can the European Cycle of Death be reversed?

The Path Forward

— STRUCTURAL REFORMS

— STIMULUS

— LEADERSHIP

This is the ideal scenario: a leader emerges with a clear plan and has the broader public’s backing to move ahead. The European people will be ripe at that point to first understand what is needed and second be ready to go through it.

The plan would be a Make Europe Great Again-style plan, but with a European spin. I’m not sure talks of MEGA (i.e. Europe Greatness) would be convincing to Europeans at large — but there will be a need for leaders to stand behind it.

The Grand Master Plan required to save Europe would go something like this.

1) True Structural Reforms

There needs to be actual competition between member states for things to pick up pace. Putting everyone on a level-playing-field with top-down EU directives and then expecting them to all comply to the T is futile. I think in many instances, each country should choose its own way forward.

Take an example: Investment managers and Funds. Brussels and EU Regulations in that sector have killed that business with their complicated regulations and costly compliance structures.

The Master Plan should focus on de-regulation and a facilitation of business. If it does that, business activity will pick up and gain momentum.

Regulating for the sake of regulation — which is something Brussels is definitely guilty of, is a dead end.. I am sure you agree that the attached plastic bottle cap and endless “Accept All Cookies” popups whenever you visit a website isn’t exactly innovation. In fact, in typical EU fashion, it mostly results in a waste of time and resources.

I for one have managed to spill water all over the seats in my car because the attached cap makes it difficult to seal the bottle well, and anyway no one ever reads the disclaimers about cookies!

Imagine how much low-hanging fruit there is to work on in sectors of the economy that actually matter.

2) STIMULUS — The Differential between the EU and the US

The thing with stimulus is even if one could argue it’s wrong economically, (unintended consequences and all) you have to do it just because everyone else does it. It’s like a stimulus race!

And the “stimulus differential” between the US and the EU since the GFC has been massive. The Americans freely stimulated their economy with generous monetary policy and lax fiscal spending while the Europeans basically did the opposite.

Why, Philo?

Monetary policy and stimulus was only executed to pull back nations from the edge of the cliff. Fiscal policy was only extended for to keep “socialism” alive..

So while the US was using those two levers of stimulus to strengthen their economy and extend their economic supremacy lead against the rest — Europe was merely dragging its feet hoping to stay alive..

WHAT DID WE EXPECT???? 🙄

So, how can Europe bridge the gap now?

THE EUROPEAN BAZOOKA! 💥

- FISCAL

Every country has to fiscal spend a certain amount of GDP every year towards purely growth investments. They can find the money from somewhere else or cut spending that has a negative ROI to make up for the budget shortfall.

—> This will not only be a structural and political requirement, but something backed by the people’s of each country. If there is popular backing, it will happen with no excuses.

- MONETARY

To opine on a monetary policy route is harder because it depends on how markets react — the Euro, Sovereign Yields, Inflation etc. But the ECB together with EU Institutions must have a pro-growth mindset and backstop big and transformational investments with their balance sheet…

What?!?!? Buying bankrupt sovereign paper to bail out the Euro is somehow better???

3) LEADERSHIP — We have Zilch.

But nothing can stick without the secret ingredient — leadership and an overwhelming sense that “we” are going places. It’s the ingredient that will make everything stick.

EU member-states must realise that “no man is an island” and that they must reverse their strategic retreat from the European Project (and Dream) if they want to see it survive.

UNTIL I see this happening, I will remain deeply skeptical about any major recovery in Europe. Yes, there may be attempts to stimulate the economy with measures like the ones taken in China last September (Piece here) but I think the recovery will eventually hit a wall.

BRINK AND BANK

This is a recurring mental model we talk about here on Philoinvestor — which I learned from George Soros. It reasons from the POV that our rulers only muster the political will to take DRACONIAN measures only when we go to the brink.

And when that happens, we move back from the brink. This can be a very profitable setup when you trade it properly.

—> More context on brink and back from my Soros piece here.

Are we approaching the brink in Europe? HOLD THAT THOUGHT 👇

The EU as a vassal of the United States

Excerpts from Battle for Europa

Philoinvestor

Philoinvestor

The EU went from having an unfair but acceptable hegemon (Merkel) and a semi-sustainable direction — to having NO hegemon and a self-destructive direction.

Today, the people of Europe disagree with the path the bloc is taking, and they are expressing that in the polls.

This rhetoric of escalation is not benefitting Europe one bit. Europe’s combined military capabilities have been on the decline for decades while the fiscal situation of the Euro Area is too weak to handle a ramp up of military spending.

Excerpt from Europe Stopped Dreaming 👇 commenting on this thread here.

Does the war in Ukraine and the broader conflict with Russia benefit Europe? Absolutely not. Is said conflict tearing Europe apart? Absolutely.

Then why is Europe going ahead with it?

Europe has been turned into a vassal by the US and is being pushed around. The US doesn’t care what happens to the EU and Europeans (that should be obvious by now). Europe will eventually implode if it doesn’t stand up to the American bully.

And so this viral thread on X here forgot to mention this basic conflict of interest, that the US doesn’t want a strong EU at par with the US. And until the EU stands up to the US, nothing will change.

Note: I wax political not because I want to — but because the political layer is vital to understanding the matter at hand.

Once we realise that imperfect understanding is the human condition, there is no shame in being wrong, only in failing to correct our mistakes. —George Soros

CONCLUSION — TL, DR.

And so yes, Europe is approaching the brink — but I am not sure if Europe (or anyone in Europe) can/will do anything to pull us back from the brink sustainably.

The European ship has too many anchors pulling it down, and if those anchors aren’t removed — this ship is going DOWN.

In the meantime, I remain super bearish on the common currency and stay intellectually open in seeing it drop much further. I see no European Messiah in the horizon and will re-assess my thesis when I see things changing.

Having said that, I expect catalysts to come out of Europe within 2025…

We will be here for them.

Sincerely,

Philo 🦉