Is the Euro here to stay?

Forming the hypothesis for a disintegration of the Eurozone.

“There are decades where nothing happens; and there are weeks where decades happen.”

– Vladimir Ilyich Lenin

Much has been said about the viability of the Euro and the EMU1. In this essay I will discuss the formation of the EMU, the dynamics that regulate its existence, important historical developments and the potential for its disintegration.

The development of the EU and with it the idea of the Euro as its common currency was viewed positively from the countries of Europe. The positive sentiment towards the European idea enabled the political will and mustered the tools and co-operation required to make it a reality.

Entry into the Union and adoption of the common currency happened in phases, allowing for modifications to adapt to challenges. Skeptics used the lack of fiscal union to point out the Eurozone’s weaknesses, concluding that the EMU was flawed and therefore bound to fail.

During the acute phase of EU growth the environment was supportive. Inflation was low, growth was high, globalisation was in full swing and there was a common view among candidate countries that they needed to be part of a greater trading bloc and not be left behind.

The adoption of the Euro led to a convergence of interest rates across Eurozone countries. Suddenly Italian, Spanish and German sovereign bonds were denominated in the same currency. This allowed countries to borrow cheaper, which helped economic growth and pushed for a general feeling of prosperity within the Union. Confidence was running high.

Sentiment continued to be positive until the financial crisis of 2008, which uncovered weaknesses in the union and resulted in multiple bank bailouts. In late 2009, the European debt crisis kicked off with revelations that Greece was falsifying its fiscal figures.

The Greek financial crisis had far ranging consequences for the Union. It gave solid proof that serious flaws exist within the EU, that new structures need to be created to deal with these crises, that strong political will is a required ingredient to move forward and that serious conflicts of interest exist between domestic and European politics.

Financial markets reacted to this loss in confidence causing yields to spike, further feeding the idea that Greece can never pay back its debts. As this Greek tragedy was unfolding the leading countries of the EU dragged their feet - even in the face of clear signs that the solution for Greece was failing. The delay allowed the crisis to fester.

These “leaders” did not want to seem soft on Greece in the eyes of their people (i.e. voters) back home. And by doing so they uncovered a clear asymmetry, that they were choosing a path for Greece that they would never choose for their own people. The path of painful austerity.

Time continued to pass, with dropping GDP (and by extension tax revenues) and an increasing debt burden. Discontent within Greece grew and in 2015 a leftist government came into power.

The newly-elected PM Tsipras talked a hard game about how he would force the EU to play by his rules. The Europeans however wanted to make an example of him. No debtor EU nation could get the idea that it can revolt against the powers that be in Europe. The example had to be set.

While the Greek episode and European debt crisis were unfolding (2009 - 2015), other nations were also in trouble. Cyprus, Spain, Portugal and Ireland needed a bailout as a result of the European debt crisis.

Many advised for a Greek default and Grexit, and to an extent financial markets already started to price it in. Other believed that the Euro was irreversible and Greece had no choice.

Arguing between the two is not the focus of this essay - but dynamics were shifting and the EU morphed from a voluntary union of equals to an involuntary union of unequals. Germany and the other creditor nations stood on one side and the debtor nations stood on the other. Financial conditions were continuing to worsen with yields blowing out specifically in the bonds of debtor nations. Perversely, German bond yields were compressing, enabling Germany to benefit from the crisis.

After the first Greek bailout was failing, Europe agreed to the Greek PSI2 which was a 50% haircut on debt owed only to the private sector. The PSI was communicated as a success for Greece but Greek and Cypriot banks that owned massive amounts of Greek debt suffered serious losses from it.

Greek banks were swiftly recapitalised with the help of the EU, but Cypriot banks were drowning in a loss in confidence that resulted in bank runs. Proclamations from Germany that the haircut was not out of the question surely did not help the situation.

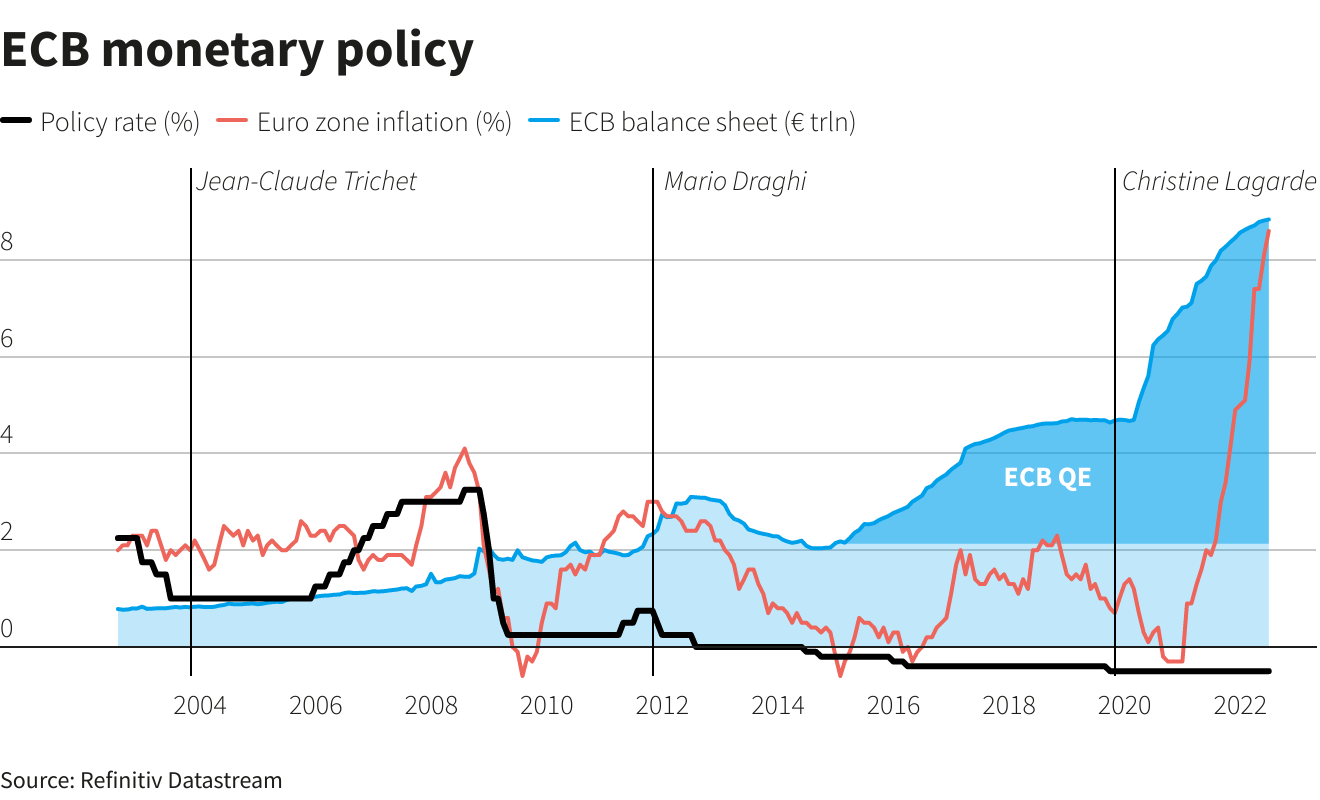

Sentiment shifted in July 2012 with Draghi’s “Whatever it takes” speech to save the Euro. Markets saw that speech as a major policy shift and trying to arbitrage the present with the future, partially did Draghi’s job for him.

Two months later, the OMT (Outright Monetary Transactions) programme was approved by the ECB’s Governing Council with only one vote against, that of the Bundesbank Governor.

After Draghi's speech and the introduction of OMT3, things entered a calmer phase resulting in falling bond yields, lowering unemployment and economic growth.

In 2013, Cypriot banks were receiving ELA (Emergency Liquidity Assistance) from the ECB with no issue until March 21st 2013, as the ECB expected Cyprus to enter into a bailout program after the Cyprus presidential elections. The only problem was that the bailout included a bail-in of depositors. This development was received as unacceptable from the Cyprus side and the bailout package was put to a vote in parliament.

The Cyprus parliament voted negatively (the ruling party did not vote4) to the bailout offered by the institutions. As a result of that, the ECB decided to terminate the ELA and demand its full repayment5. These overly harsh actions resulted in bank resolutions, deposit haircuts and a massive ELA balance still outstanding.

Suddenly, one euro in the Cyprus banking system had a different value from one euro in another Eurozone banking system - and one euro in a Cypriot bank had a different value from one euro in another Cypriot bank.

The totality of deposits in Laiki above €100,000 were fully haircut and 50% of deposits in the Bank of Cyprus above €100,000 were converted into equity (now 90% out of the money). If Draghi’s ECB had not extended so much ELA (65% of Cyprus GDP) the numbers would be completely different. ELA allowed fleeing depositors to recoup 100% of their money while those who stayed payed the price for both.

The narrative being pushed by the Germans was that Cyprus was a corrupt tax-haven, with a banking system that existed mainly to pay Russian oligarchs high interest rates, and that the deposit haircut would mainly hurt them and not Cypriots. Never mind that Deutsche Bank has been fined half a billion Euros for these same reasons6 .

In January 2015, Draghi announced a Quantitative Easing programme to inject liquidity into the system and achieve the inflation target of 2%. Growth and inflation was running below target and the ECB had to bring out the big guns to jumpstart the system. The market was buying into Draghi’s narrative and the Euro crashed vis-a-vis the Dollar reflecting negative interest rates and a massive expansion of the ECB balance sheet.

Things entered a calmer phase in the Eurozone until covid struck. The pandemic not only unleashed great inflationary forces, it did so at a time of near-zero interest rates. Sovereigns went deep into budget deficit territory by borrowing to support households and businesses during the pandemic.

The massive inflationary spike eventually forced the ECB to to start rate hikes. The ECB main deposit facility is currently at 2.5%, from -0.5% a few months ago. With current inflation rates it still has a few points to go.

Now, over indebted EU sovereigns will have to pay a higher interest rate to finance their increasing debt burdens. And all this on top of a growth problem.

You see, Europe is no longer the centre of the world. Rather Europe is in the late stages of its growth cycle. Growth is slowing, the populace is self-entitled and governments are overly taxing and regulating what growth and innovation is left.

Take energy security. EU imports over 50% of its energy needs. This is a fundamental weakness which blew up in the Eurozone’s face when Russia invaded Ukraine.

On top of that, Nordstream 1 & 2 were hijacked and completely destroyed - leaving Germany exposed and in need of a complete makeover of its energy infrastructure.

How did Germany and the EU respond to this cataclysmic event? They introduced a windfall tax on oil & gas producers and electricity companies. The rhetoric was that these companies should not profiteer on the war, and that these “wartime profits” should be returned back to the governments. EU leaders feel that they have solved their energy-related problems, and for now it seems so.

But you don’t solve long-term structural problems with patchwork solutions. These decisions will come back to haunt the EU.

The EU should incentivise producers to invest, not disincentivise them. Besides, when producers were making losses during bad energy markets did anyone go to their rescue? Of course not. It was up to free-market economics and market forces to decide whether they survived or perished.

Now when times are good and they can make a profit and keep investing - the government goes to them for a bailout. Producers will now prefer investing outside the EU rather than within, moving Europe into further energy insecurity. No wonder economic growth is lagging in the Eurozone.

Looking at the complex nature of the Eurosystem, it is easy to believe that the Euro is irreversible. Maybe this was one of the reasons why the architects of the EMU created the common currency, to create a knot that can never be untied. A sort of gordian knot.

Maybe the Euro’s gordian knot can never be untied, but it can certainly be cut. And the more things that divide the EU the closer we get there. Years ago political discussion in the EU was focused around the creation of a common treasury and choosing between austerity or growth as a way out of indebtedness.

Now all of a sudden Europeans can’t agree on anything. This is a list of the major political rifts within the EU.

- Sanction Russia or not?

- Go to war with Russia or not?

- Pro-NATO or not?

- Support NATO expansionism or not?

- Support European Union expansionism or not?

- Pro-EU or not?

- For a multipolar world or for a Western-led world order?

- Controlled immigration or uncontrolled?

- Sound money or Quantitative Easing and endless Keynesianism?

- Nuclear Energy or anti-Nuclear?

- Green Energy transition subsidised by the state or free-market economics?

Could these dogmatic differences result in the first member to exit the Eurozone? Within the EU there are ruling political factions and dominant political ideas. The problem is that these ruling factions force their ideas on the rest.

The implicit threat is that breaking from the prevailing idea makes you opposed to Europe and therefore dangerous - and so most leaders in the EU just go with momentum.

You are not allowed to have your own ideas on how to run things. If you have opposing views, we will hurt you. Recently, Ursula von der Leyen implicitly warned7 the leading Italian coalition before the elections, that if they break from EU direction they will be punished.

But there is a consequence to European meddling into domestic politics. Voters have started to consider EU political dynamics when casting their vote - and there are shifts taking place.

In Germany, the anti-EU AfD8 (Alternative für Deutschland) party is currently at 15% in the polls, from 10% on the day of the Russian invasion and 4% just 10 years ago. The European idea is losing traction and discontent is growing.

You can be sure that as the chasm on these key issues grows, and economic performance suffers - cries domestically against the EU will only grow.

Each country has it own unique identity, history and culture - all the things that make it unique and special. Forcing these countries to comply top-down with all the regulations conceived in Brussels and Berlin ignores this.

It’s true that the foundations of the EMU have been seriously strengthened since the financial crisis of 2008. The formation of the ESM now allows a member state in financial trouble to apply for financial aid.

The country under adjustment would have to complete a number of reforms and comply with a number of requirements to receive the financial aid, and then it actually has to pay back the debt.

The European debt crisis that kicked off with the Greek crisis was the reason to form the ESM - to deal with the possibility of more crises.

Through the multi-year long saga between Greece and the EU institutions, and the German government taking the role of the strict hegemon, we saw what happens when conflicts of interest play a decisive role in shaping the course of events.

The Germans and their friends needed to appear tough to their citizens. The rhetoric being propagated was that Greeks are lazy and that they are in debt because they mismanaged their finances.

Sure, government overspending (as well as falsification of its financial figures) played a part. Just like in every other country in the world. But the people are not to blame here, only the politicians.

And who was the strongest communicator of this strict message? Germany and its leaders at the time, Angela Merkel and Wolfgang Schäuble9 (who in 1999 admitted to accepting cash contributions for his party from an arms lobbyist).

Germany — a country who owes hundreds of billions in reparations to Greece as a result of the Second World War and the Nazi Germany occupation of Greece was giving lessons to the Greek people on how to run their country.

A country with an endless list of political and financial scandals of epic proportions, some of which cost Greek finances billions10 was suddenly without blame.

Is this the idea of Solidarity that Europe speaks of? That we can forget and ignore the past whenever it suits us to keep our political party strong at home? This is not strength, this is a weakness right in the heart of Europe.

In the end, Grexit was barely avoided - but will the next EU member in crisis be willing to go through the same painful adjustment that the Greeks went through?

It is important to note that Greece’s debt ballooned to such levels not only from traditional budget deficits, but from large military expenditures as a consequence of their conflict with Turkey.

Both Greece & Turkey are members of NATO, and all the weapons that Greece bought are from American, French and German manufacturers. Again, those conflicts of interest. The creditor nations like Germany were quick to criticise the debtor nations and point out their mistakes but wouldn’t recognise their own.

So the next time an EU member is in the crossroads of staying in the EU or venturing out on their own - they will weigh the benefits and the costs and make their decision.

The moment that benefits don’t clearly outweigh the costs, they will leave. In fact, it doesn’t even have to come to that point. Markets will see the potential for such a scary prospect (like they did for Greece) that they will front run future developments and in doing so create them.

At that point there will be no whatever it takes speeches or quantitative easing bazookas to save the system.

As when Britain abandoned the ERM and the US abandoned the Bretton Woods agreement, authorities will accept the new state of affairs and act to catch up to them, not prevent them. When it is finally accepted that the first country has left the Euro, calculations will be made about how to untangle the Euro’s gordian knot. There will be some cutting and some untying but finally the knot will be removed.

It is possible that the country to exit will have two currencies in circulation during the transition process, and the exchange rate will be allowed to float between the Euro and the new national currency.

The country’s sovereign debt will be re-denominated into the new national currency, removing the currency mismatch issue. The exit country’s right to do that is debatable, but those who take issue will have to take the matter up in court.

Ultimately, the exit country’s financial future will depend on the decisions it takes after the exit. The exit country must implement structural reforms, cut and rationalise government spending, incentivise its citizens to work hard, implement a fair tax policy, attract foreign investment and deregulate sufficiently to allow market forces to do their job.

If this is done, regardless of the chaos or confusion that could happen immediately after the exit - the country will be back on its feet in no time.

While I am not predicting that the expectations I lay out in this essay will surely happen, if the EU continues in its current path they will be unavoidable.

The underlying trend for the European idea started out positively and was later reinforced when the system was saved from the debt crisis. Now with the growing rifts and divergences the trend is losing steam and turning down.

Integration is a dynamic process and if it stops moving forward it starts moving back. If common ground is not found, reality will further diverge from the European idea until the gap is too wide to sustain.

https://economy-finance.ec.europa.eu/economic-and-monetary-union/what-economic-and-monetary-union-emu_en ↩

https://www.esm.europa.eu/publications/2012-private-sector-involvement-greece ↩

https://en.wikipedia.org/wiki/Outright_Monetary_Transactions ↩

https://www.ekathimerini.com/news/149473/cyprus-parliament-rejects-haircut-bill/ ↩

https://www.dw.com/en/deutsche-bank-fined-425-million-over-suspicious-russia-trades/a-37343153 ↩

https://tfiglobalnews.com/2022/11/04/meloni-has-a-plan-to-save-europe-but-it-has-an-ursula-von-der-leyen-problem/ ↩

https://www.kai-arzheimer.com/afd-right-wing-populist-eurosceptic-germany/ ↩

https://en.wikipedia.org/wiki/Siemens_Greek_bribery_scandal ↩