Valaris, literally striking oil.

Offshore Drilling Company. Investment opportunity in the equity and debt.

UPDATE: I wrote an update on the company in March 2023 here.

And then another one here.

In early 2023, I explained in this now-released piece why I didn’t like Transocean.

In late 2024 I wrote “A State of Offshore” here.

The offshore drilling sector is still being viewed negatively by investors as Bankruptcy and Restructuring is not what you want to hear when you are the typical scared investor.

This opportunity is for the more business-oriented player. Read below.

Valaris is the result of the merger between Ensco and Rowan. Ensco acquired Rowan Companies plc in 2018 for $2.38 billion in an all-stock deal. Ensco had already acquired Atwood Oceanics in 2017, so the combined Valaris is made up of Ensco, Rowan and Atwood.

Severely hurt from the 2014-2015 oil price bust, the offshore drilling sector was dealt a final blow when covid-19 struck in early 2020.

Oil companies starting pulling back from new projects after oil peaked in 2014, and this negatively affected demand for offshore drilling. The offshore sector was heavily indebted at the time, and companies started restructuring their debt as well as retiring and cold-stacking rigs.

Removing rigs from supply does not come without a price, as stacked rigs continue to incur expenses for storing and interest expenses on debt continue to accrue as the debt financed assets brings in 0 in revenue.

While offshore drillers were tagging along trying to work their way out of the mess they put themselves in, the pandemic strikes, resulting in another round of oil price drops and cancellation or suspension of oil projects that would require offshore rigs.

Valaris filed for bankruptcy protection (Chapter 11) in August 2020 in an attempt to restructure its affairs and cancel $6.5 billion in debt. The NYSE suspended Valaris shares immediately and delisted them in the same month.

In March 2021, the court approved Valaris’s reorganization plan allowing the company to emerge from bankruptcy debt free and to relist its shares on the NYSE.

What does Valaris look like today?

Net debt of $0 million with a cash balance of $600 million as per second quarter of 2021, and long-term debt of $550 million via a bond issue.

The Bond Issue

8.25% Senior Secured Notes maturing April 30th, 2028. The issuer has the right to service the debt by a Payment-in-Kind (PIK) for the life of the note, which carries an interest of 12%. For a half cash, half PIK debt service, the interest is 10.25%.

The Warrants

April 2028 expiry, $131.25 strike price (currently trading at $36) warrants for a total of 5.6 million new shares, or about 7% of currently issued shares.

The Fleet

Valaris owns 8% of the global rig fleet.

The active fleet is operational and generating positive cash flow for the company. The leased fleet is also returning cash flow for the company in the form of bareboat charter agreements to ARO (more on that later).

The problem however in the offshore drilling sector is when you have paid a lot of money to buy offshore rigs and are subsequently forced to stack them because there is not enough work around. Unfortunately, stacking does not come cheap.

Stacking comes in two forms, cold and warm stacking. Cold stacking, also known as preservation stacking, comes with upfront costs of several million per rig (one time cost), and daily operating costs of less than $10,000 per day.

To bring back the rig into operation takes 3 to 4 months and reactivation costs which range from 10 to 20 million for jackups, and 30 to 45 million for drillships. Reactivation costs are somewhat of a guess because you can never know how much the rig will deteriorate with time. That is the big risk of cold stacking.

Some offshore drilling companies willingly understate their expected reactivation costs to show a better face to their stakeholders and to the market. They are kicking the can down the road, so to speak.

Warm stacking carries daily operating costs of $40k to $60k per day depending on the type and age of the rig. The price is high but it comes with the peace of mind that your rig is well maintained and operational.

There is also a middleground in stacking, called smart stacking (or semi-stacking), where drillers try to save costs by making stacking more efficient by bringing the costs of a warm stack down while avoiding the disadvantages of cold stacking.

The Valaris fleet of 18 cold stacked rigs today cost the company ~$60 million per year (~$9,000 per rig per day). That seems like a lot of money, but in the grand scheme of things it is a small amount to pay for the chance to bring back those rigs in operations and earn billions in revenue going forward.

What kind of optionality is this??!?

Offshore drillers and other capital intensive businesses (i.e. shipowners etc.) speak of “optionality” embedded in their business models. In simpler words, they mean that the assets they own could one day earn a lot of money when (and if) the cycle turns.

But that optionality comes at a cost. In the case of offshore drillers it is the yearly cost to keep those assets stacked and not retire them once and for all. Let’s call that the “premium” one has to pay to be long that “optionality” that companies talk about in their presentations and earning calls.

There are a lot of issues with that. Firstly, the assets were already bought and paid for, and now they cost even more every year for the right to simply own them.

In other words, in a low cycle environment where rigs are in oversupply, a company can find itself having to suffer premium every year to continue owning an asset that it has previously already purchased. That’s not exactly how options work, but I digress.

You forgot to mention negative optionality.

If the cycle doesn’t turn in time, allowing rigs to find employment at reasonable enough rates to fund the reactivation costs required to bring them out of cold stacking (if they are indeed cold stacked) and generate a healthy profit, then the company is simply throwing good money after bad by continuing to pay for those option premiums.

In the case of indebted offshore drillers; the negative optionality is even larger as debt servicing and covenants will make it harder for the company to remain flexible during the downswing. Hence the many bankruptcies in the sector since 2014.

Taking the guesswork out of it.

In the case that the cycle indeed stays low for the foreseeable future, Valaris and the offshore sector will start retiring more and more rigs further constraining rig supply. This is the process which happens in sectors where supply currently surpasses demand and must go through a period of self correction. Examples include dry and wet shipping, commodity producers etc.

Retiring rigs would mean that capital previously spent to acquire those rigs is now almost entirely written off. Those that paid high prices for these assets (let’s call them oversupply assets) are now deep out of the money on their investment. Let’s just call it a bad trade, now what?

Now, those that pay lower prices for those same oversupply assets are in a much better position than those that paid full prices.

What is the active fleet worth?

The value of the active fleet is the discounted cash flow it can generate over its lifetime. But for simplicity’s sake, let’s leave out the discounts for now and try to assess how much cash flow we can earn from these rigs during their useful lives.

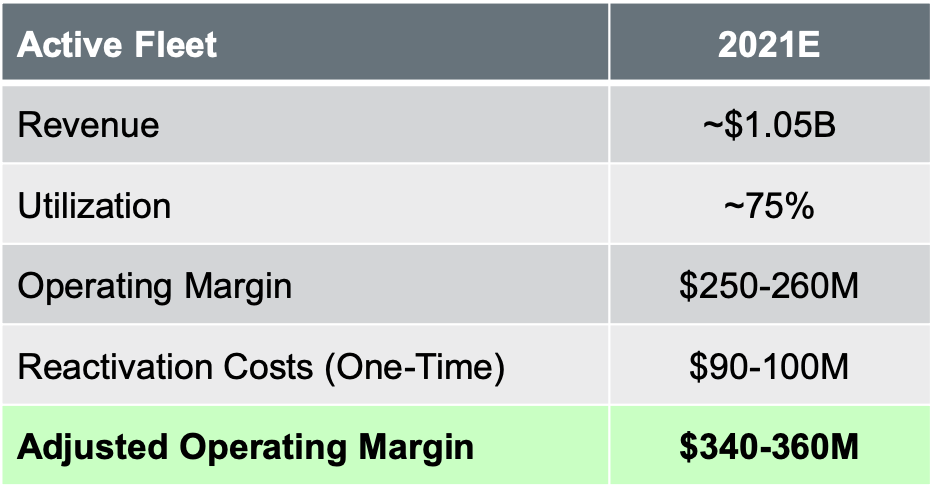

The company is guiding 2021 total revenue of ~$1 billion and a utilization of 75% for the active fleet (which includes warm stacked rigs). With these figures, the active fleet generates ~$350 million in EBITDA at the rig level, before onshore supports costs and general and administrative expenses (about $200 mln per year in total).

The active fleet is currently comprised of 31 rigs, of which 24 are jackups and 7 are floaters. For the first half of 2021, day rates for jackups and floaters were ~$100,000 and $200,000 respectively.

Day rates are anything but stable; on year end 2020 the backlog for jackups was $740 million at an average day rate of $86,000, and for floaters it was $164 million at an average day rate of $188,000. By mid-year 2021, floater day rates moved up 30% to $245,000 while jackups did not budge.

Considering that the market is in a low cycle environment with low fleet utilization across the board, what is a conservative average day rate to assume going forward for these assets? A more “normalized” environment so to speak.

Assuming the same utilization of 75% and a 20% increase in day rates for jackups and floaters relative to year end 2020, we get ~$100kd (kd means thousands per day) and ~$225kd for jackups and floaters respectively. Considering that the business model has significant operating leverage, we assume that the bottom line increases twice as fast as day rates. i.e. A 20% increase in day rates results in a 40% increase in EBITDA generation.

Therefore, the active fleet can earn $350mln * 1.40 = $490 mln in EBITDA per year in a more normalized day rate environment. The assets have significant remaining useful lives but using a back of the envelope calculation we assume that the active fleet can trade at these metrics for a mere 5 years.

—> Assume $2,500 million in total cash generation for the active fleet.

What can the leased rigs earn?

Valaris also leases rigs to ARO in bareboat charter agreements and they guide for $75-85 in operating margin for 2021. Valaris receives an undisclosed percentage (it’s more than 50%) of rig EBITDA as remuneration for the bareboat charter.

Assume that this cash flow is stable and the company will at least generate this amount going forward.

—> Assume $80 million in cash generation for the leased rigs per year.

What can the stacked fleet earn?

For the moment, the stacked fleet does not earn anything. Actually, as explained above, it costs the company every year to maintain the stacked rigs; incurring carrying costs every year of $60 to $70 million per year. This is the price the company has to pay while waiting for better market conditions to charter these rigs out.

The stacked fleet has an average age of 14 and 8 years for jackups and floaters respectively, which means they have significant useful lives ahead of them.

In a more normalized market environment, the stacked fleet can generate $200 to $300 million per year.

—> Assume $200 in cash generation for the stacked fleet per year.

All in all, Valaris can earn under a normalized scenario, $2.5 billion from the active fleet, $80 million per year from leased rigs and $200 to $300 million per year from the currently stacked fleet when and if they ever come back to the market.

Is that it? Enter ARO Drilling.

Together with the Rowan Companies acquisition in 2018, Valaris also obtained a shareholding in ARO, a joint venture owned by Valaris and Saudi Aramco under a 50:50 ownership split.

ARO has significant upside as ARO’s main customer is Saudi Aramco, the strongest and biggest energy company in the world (owned by the Kingdom of Saudi Arabia).

ARO intends to build 20 jackups over the next 10 years. ARO expects to pay for these newbuildings via cash on hand and third party financing. This offers significant potential upside for Valaris going forward.

Currently, ARO guides 2021 EBITDA of $105 to $110 million. Half of that accrues to Valaris.

—> Assume ~$50 million in cash generation for Valaris’s holding in ARO.

Rounding it all up.

Active Fleet, $2.5 billion in total (5 good years)

Leased & Managed, $80 million per year

Stacked Fleet, $200 to $300 million per year

$50 Equity in ARO, $50 million per year

Valaris is currently selling for a market capitalization of $2.68 billion (75 million shares at ~$36 each). Valaris’s market capitalisation is equal to its enterprise value as the company has net debt of zero.

From the table above, one can see that the company can generate total EBITDA (before onshore operations) equal to the total of its current market cap simply by 5 good years in the offshore drilling market.

What if the market turns up and demand for floaters and jackups increases, allowing the stacked fleet to come back to trading?

What about the value from the 50% equity in ARO and the cash flow from the leased and managed rigs?

The value that the company can generate under a more positive scenario is tens of billions going forward.

But what about the potential downside?

In a prolonged low cycle scenario, Valaris will start retiring its stacked fleet and thus reducing the carrying costs it incurs every year. I would not be too concerned as I believe the current valuation does not price in much value to be extracted from the stacked fleet going forward.

Conclusively, I believe an investment in Valaris offers a low risk, high potential reward investment. For a further explanation into my thought process on investing by positive asymmetry read this.

Fun fact:

The famous Greek shipowner Aristotle Onassis tried to strike a deal with the Kingdom of Saudi Arabia in the 1950s to be the sole shipowner to transport Saudi’s abundant crude oil. The British and U.S. governments, as well as rival shipowners were alarmed by this deal and by their collective efforts the deal fell apart as it was cancelled in 1955.

Fun fact 2:

Saudi Arabia has announced “THE RIG”.

Further reading:

https://www.nytimes.com/1975/12/19/archives/onassis-oil-deal-reportedly-upset-with-cias-help.html