Greggs

Pulling all the right levers.

Greggs PLC (GRG.L) is the fourth addition to the NED Index.

Greggs is a bakery and FTG (food to go) chain with shops across the United Kingdom. It’s listed on the LSE and is part of the FTSE250 Index.

The company has experienced rapid growth, with 2024 being the first year it crossed 2bln GBP in revenues.

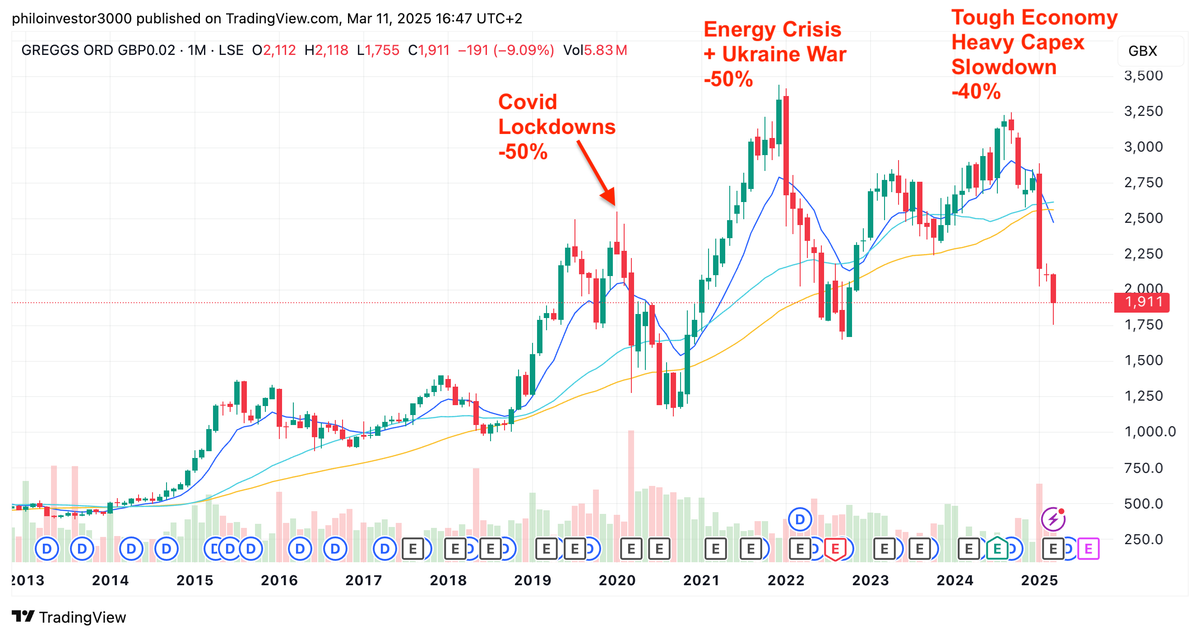

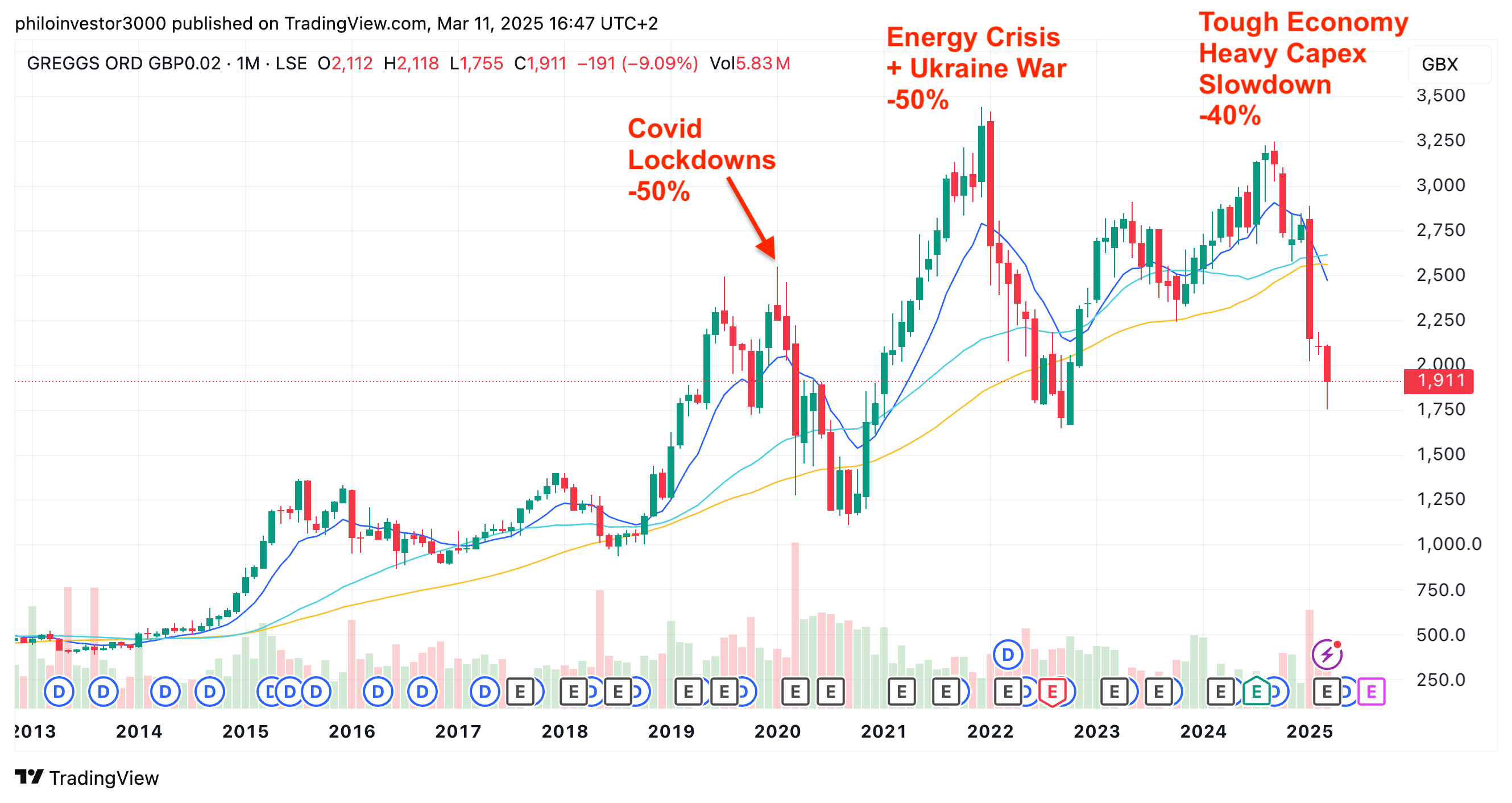

For some historical context…

In 2021 the company set out to double sales by 2026.

This created the need for extra infrastructure (still ongoing!) to support growth, as well as new stores every year — including relocations and refurbishments of existing stores.

In mid-2024 the share price rally was stopped in its tracks, with shares crashing ever since ever since — with a massive drop in early January as the company reported a slowdown in LFL (like-for-like) Sales growth. This was due to a challenging economy in H2 ‘24 and warnings of “further overall cost inflation”.

This was the start of a repricing of Greggs shares and the market readjusting its view of the company.

Note that in 2016 the company commenced its transition from a traditional-regional bakery model where every site made every product — towards a consolidated, centralised approach of production.

The company’s manufacturing footprint today boasts 9 manufacturing facilities, each one specialising in specific products.

Greggs is a suitable addition to the NED Index as it is a simple, predictable and cash-flow generative business that is (obviously) also a dividend payer.

For NED, we are simply looking for superior economics expected to remain so for the considerable future — and we want to pay a reasonable price for the privilege of owning them. Simple, but not easy!

Pulling levers for growth

Greggs seems to be everywhere across the UK, right?

Is there still any growth left? Oh yes.