European Energy Or European Defence?

Vermilion Energy Vs Rheinmetall. Updates on Glencore.

Let’s start with Glencore to get it out of the way before comparing the opportunity set in Rheinmetall AG and Vermilion Energy.

We sent out a note on Glencore almost one year ago — concluding with the below.

For a commodity-related capital-intensive cyclical company, that buys back shares at any price, while China is slowing down and the EV theme is facing a wall (I believe) — one needs to be very careful about the prices he chooses to pay.

……….To make money from this company, one needs to buy at deep discounts (the margin of safety). For me, we are not there yet.

Sure enough, Glencore is down ~25% since then and reported results this week. Y/Y EBIT was down 33% to $7bln-ish while Net Income swung to a $1.7Bln loss, from a $4.3Bln profit.

Now go back and read the excerpt above (as well as the piece) to understand the how and what behind my thinking. My parting thoughts is that Glencore is more or less a capital-intensive, cyclical and levered play on energy and commodities in general.

—> Why would you buy after the binge is reversing? Don’t be stupid, as they say! 🌳

—> With progress on the Ukrainian front and the Coal chart looking scary, it is still not the time IMHO. But we will revisit… 🦉🫡

Now, let’s analyse two current setups and compare them as investment opportunities — those of Vermilion Energy and Rheinmetall AG.

The market seems to be forgetting that the holy grail im investing is Price-to-Value, not just value.

Let’s dig in…

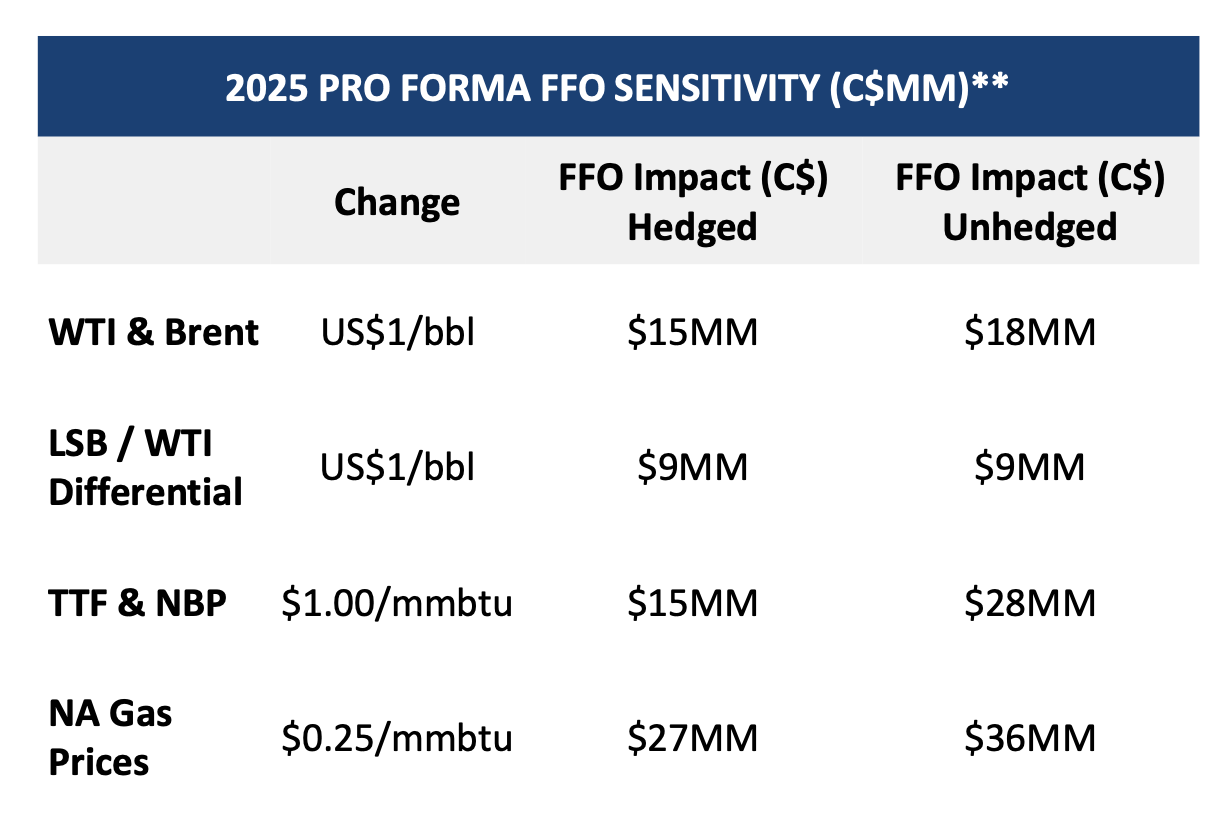

Vermilion Energy

The market hates Vermilion. Post-Covid-reopening and the Russian invasion into Ukraine — Vermilion’s European gas exposure (and Crude) promised endless cash to those who were smart enough to jump in and buy…