NETFLIX: Content is King but distribution is God.

On Netflix and the streaming wars.

Netflix was founded by Reed Hastings (“Reed”) and Marc Randolph in 1998. They started as a DVD-by-Mail service, later pivoting to a subscription model.

By 2000 Netflix was suffering losses forcing the founders to sell. They chased the CEO of Blockbuster, the biggest video rental chain at the time, for a meeting.

Months later they managed to see him but when they quoted their $50 million price tag, he saw their offer as a joke.. The duo had previously declined an offer to be acquired by Amazon in 1998.

A few years later Blockbuster started to make moves to compete with Netflix but had its own internal issues including an unsustainable debt load after being spun-off from Viacom in 2005.

The details aren’t as important but in 2010 Blockbuster filed for bankruptcy and never managed to become a worthy competitor.

The wedge, the pivot and the other pivot!

I used the analogy of the wedge in my Farfetch post, to explain how a new entrant manages to achieve a seemingly impossible goal by taking a roundabout, longer-term approach.

That’s what Netflix did in 2007 when it launched an online streaming service (the pivot). If they didn’t have the customer base, resources and knowledge from their DVD-by-mail service (the wedge) would they have managed to achieve that?

🤯 But then in 2013, Netflix pivoted again. They announced to the world that they would shift from content-aggregator to content-creator (the other pivot) when it first announced The House of Cards.

Netflix realised it had no future if it didn’t control its own content. Since then, it’s only been up.

Where is Netflix now?

With revenues of $7.7 billion (last quarter) and 222 million paid subscribers worldwide, Netflix is the global leader in streaming hands down. 🙇♂️

But things are looking bad these past few months…

What’s the narrative?

Netflix best days are behind it as the legacy content creators like Disney and HBO are gaining momentum in the space and dethroning Netflix. The content creation and distribution model can never make money because content has to be continuously refreshed and those BIG HITS are few and far between. All the streamers will now compete for viewers and content production, so the space as a whole can never be profitable. Viewers will just cancel and activate the streaming service which has the big hit of the time, only to then cancel it again for the next one.

Scratch the surface why don’t you.

Why can’t this be a case of mean reversion? Isn’t subscriber growth expected to taper off after the covid stay-at-home binge (shown above)? Is a ~1% churn not allowed in this business?

See below subscriber growth since 2018. The numbers have been huge!

In the Q4 2021 letter, management guided for a 2.5 mln growth in subscribers. Actual growth came to -0.2 mln, that was the second crash…

But it was next quarter guidance that I believe hurt the most. 👇👇👇

“As a reminder, the quarterly guidance we provide is our actual internal forecast at the time we report. For Q2’22, we forecast paid net additions of -2.0m vs. +1.5m in the year ago quarter. Our forecast assumes our current trends persist (such as slow acquisition and the near term impact of price changes) plus typical seasonality (Q2 paid net adds are usually less than Q1 paid net adds). We project revenue to grow approximately 10% year over year in Q2, assuming roughly a mid-to-high single digit year over year increase in ARM on a F/X neutral basis. We still target a 19%-20% operating margin for the full year 2022, assuming no material swings in F/X rates from when we set this goal in January of 2022.”

Besides the subscriber growth headwinds, the company is managing its ARPU (Average Revenue Per User) by raising prices in certain geographies. As a consequence, churn has gone up. But what’s ultimately better: 50% more subscribers at $10 or 30% more subscribers at $13? There you go.

Netflix is trying to balance content spent with ARPU to find the balance and achieve PROFIT maximisation, not subscriber maximisation.

What’s the potential?

Pershing Square who bought a massive position on the first crash; and quickly sold it on the second crash (!), had this to say:

The slide sums up the drivers of future growth for the company as well as its ultimate business economics. 222 million paid subs is still a fraction of the total market, but that’s not all.

Netflix is still pricing lower than it ultimately can - for the value offered they can charge much more. And Netflix has demonstrated exactly that, as show below.

Is it really a war?

Reed says competition is nothing new for Netflix. Around 2007 when Netflix entered streaming; YouTube, Hulu and Amazon Prime were also around.

The terrain has shifted since then as new entrants are competing in the space. To better understand the dynamics one must distinguish between the two types of competitors; Legacy media and Big tech.

Legacy media offerings are Disney+, HBO Max, Paramount+, Peacock and Discovery+.

Big tech offerings are Apple TV+ and Amazon Prime Video.

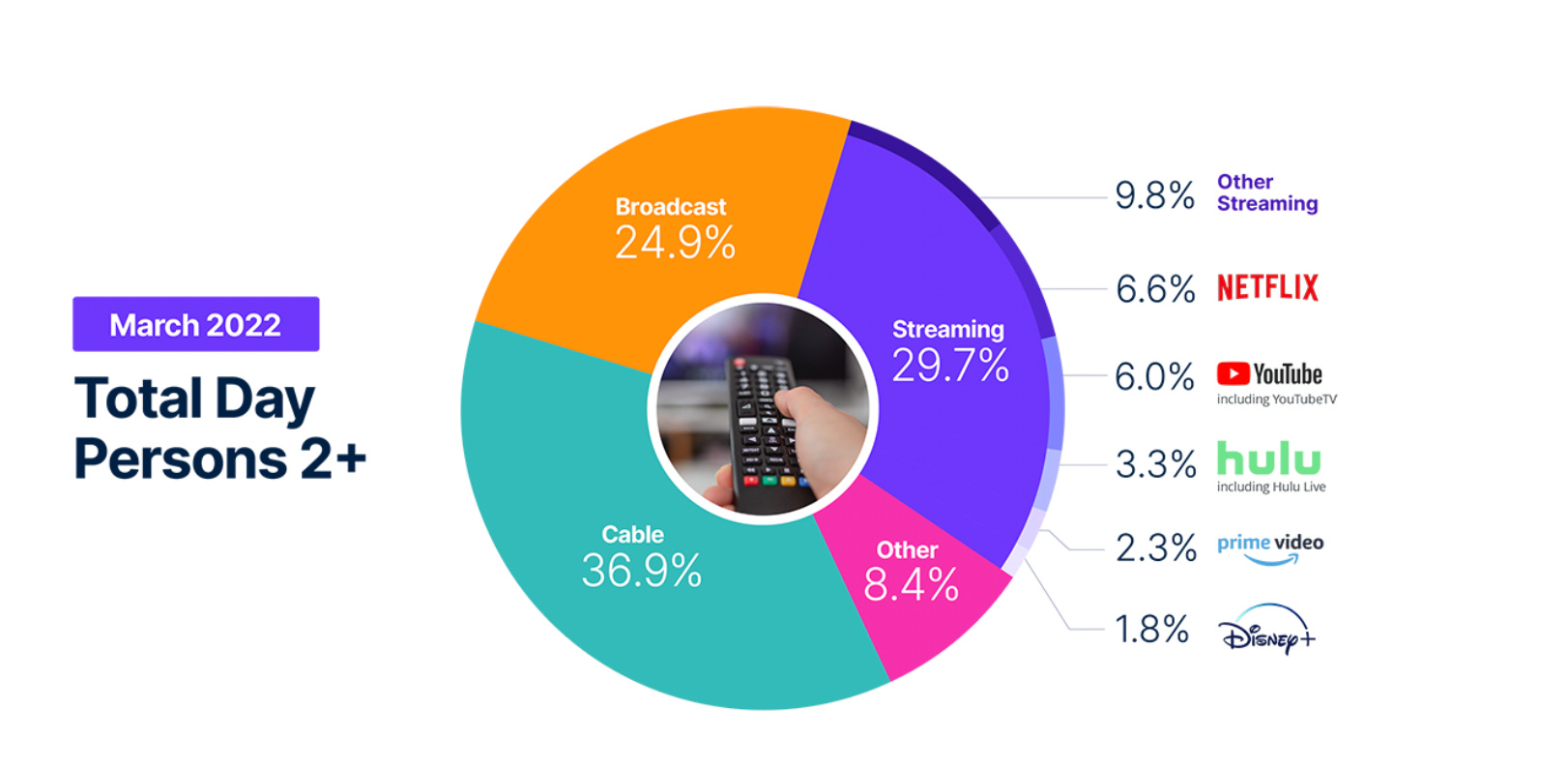

The driver for streaming is the shift from linear TV to digital. And this doesn’t happen overnight, the runway is huge. Linear TV will continue to decline very slowly. Broadcast lost 2% to 3% share per year for 25 years!

This is what U.S share of time looked like this March. Broadcast was once 100%, and was killed by Cable. Now streaming is on the up and up.

No Ads, no Games…?

Two years ago Reed was asked if they would ever considering bringing ads or games to the Netflix platform like Hulu. His response was a negative:

“It’s a funny thing because Disney is on the board of Hulu, Disney then bought Hulu, but when they go to launch with Disney+ … no ads! When you have a lot of insight into the model you make certain choices - so we are very comfortable doing no ads like Disney+ and we are going to compete on that basis.”

But Reed pivots again 👇

“Those who have followed Netflix know that I have been against the complexity of advertising, and a big fan of the simplicity of subscription,” “But as much as I am a fan of that, I am a bigger fan of consumer choice. And allowing consumers who would like to have a lower price, and are advertising-tolerant, get what they want, makes a lot of sense.”

In the second quarter of 2021 they announced they are entering games. A few months later they bought their first gaming studio later buying another.

Netflix understood that they are competing for time not only with series and movies, but for other forms of entertainment like games. They also understood that they cannot get to where they want ad free.

Ad-supported is the correct path to scale.

It’s clear that scale is the name of the game - not only content quality.

The ad-supported tier expands TAM and allows Netflix to monetise its existing library of content even more effectively. Potential users that would rather pay less for the service are now able to via this model, and Netflix still gets to monetise them via advertisement revenues.

Why is distribution the key to this business?

If legacy streamers pivoting to DTC do not manage to ramp up enough subscribers and revenue to be able to sustain their cost structures and invest for new content, they will face issues very fast.

Legacy media players are massive operations with a lot of costs and demanding shareholders that need to see cash generation. They can’t sit around waiting for the platform to ramp up. Ultimately, their heavy debt loads may be the catalyst to a changing landscape.

Warner Bros Discovery (NASDAQ: WBD), has ~$60bln in debt, 4-5X EBITDA. That’s a heavy debt load considering how dynamic this business is.

Netflix however has already ramped up subscriber numbers, generating enough revenue to sustain their content creation engine.

+100 million households use another household’s account, hence they are freeloaders. Netflix seems this as opportunity to find ways to monetise them.

Ads are certainly one way, but making account holders pay for this is another. Not all 100 million households are highly engaged but a good chunk of them are.

And what will happen to these extra monetisation dollars? They will all drop to the bottom line.

And this is why scale is the name of the game.

📺 Rounding it all up 📺

Streaming has a total market potential of ~1 billion households.

Netflix has 222 million paid subscribers and ~100 million that are freeloading, for a total of 322 million households consuming Netflix content.

That’s a 32% penetration rate with a real possibility of getting 50% of the market over the long term.

ARPU is ~$12 and moving up over time. Assuming ARPU at only $2 higher means an extra ~$450 million revenue per month. Yes, Netflix does have pricing power. Especially as they spend more on content (including games).

The introduction of the ad-supported model will increase the number of households that can afford Netflix as it will lower the absolute dollar price. Assume 50 million households at $8, another $400 million revenue per month.

I have no insight into what Netflix can earn from advertisers, as that depends on deals struck as well as hours viewed - but Paramount’s Pluto TV earns ~$2 / month from it. 50 million at $2 is another $100 million per month.

These are some of the levers that Netflix to grow the bottom line.

For those that say competition won’t allow Netflix to grow and that it’s not a winner take all market. My response is that competition has existed and will always exist. I would also add that it doesn’t have to be a winner take all market to make a profit from it.

Netflix’s success will depend on striking the right balance between pricing and value offered. Many believe rising content costs means Netflix is on a stairway to nowhere, but that’s first-level thinking.

What matters is not how much Netflix spends for content, it matters how effectively they monetise it. And having a wide and strong global base of monthly subscribers helps.

A few words on valuation💲

Netflix had sales of $30 billion and an operating income of $6.2 billion (21% operating margin) for 2021.

Market capitalisation is now at $84 billion, giving it a price to sales to 2.8x from a high of 10x.

Assuming a 30% terminal operating margin, and a doubling of revenues over time translates into a price to EBIT (operating income) of 4.7 times.

This doesn’t take into consideration other ways the company can create (or destroy) value, like buybacks or acquisitions.

Fun Fact 😂

Netflix still had $180 million in DVD-by-mail revenues for 2021…WHO STILL DOES THAT?? Of course this business line is dropping year by year, just like broadcast and cable.