The Rise of Sanakatsu サナ活

Where do we Yen from here?

Japanese Macro is always eventful – but the setup now is rather unique.

In this issue we will try to make sense of Japanese Macro in the face of a lagging and forced ZIRP unwind, amidst the rise and rise of Sanakatsu.

"Sanakatsu" is a viral youth-led cultural phenomenon in Japan surrounding the country's Prime Minister, Sanae Takaichi. Blending her name with the Japanese term oshikatsu (fandom and idol worship activities), the trend involves fans fervently adopting and purchasing the everyday items the conservative leader uses, much like dedicated pop or sports fans.

A weak opposition and the rise of Sanakatsu gave Takaichi and her LDP party the supermajority earlier this year – after Sanae called snap elections this February.

The previous PM, Ishiba, lasted for 11 months and had to grapple rising discontent with his administration and scandals related to the LDP. For context, the LDP is the longest-reigning political party in Japan and is also the party that Shinzo Abe (of Abenomics fame) led.

After Ishiba's resignation, coalition partner Komeito quit the coalition and Sanae formed a new coalition with right-wing JIP. The ruling coalition today consists of LDP and its junior partner JIP.

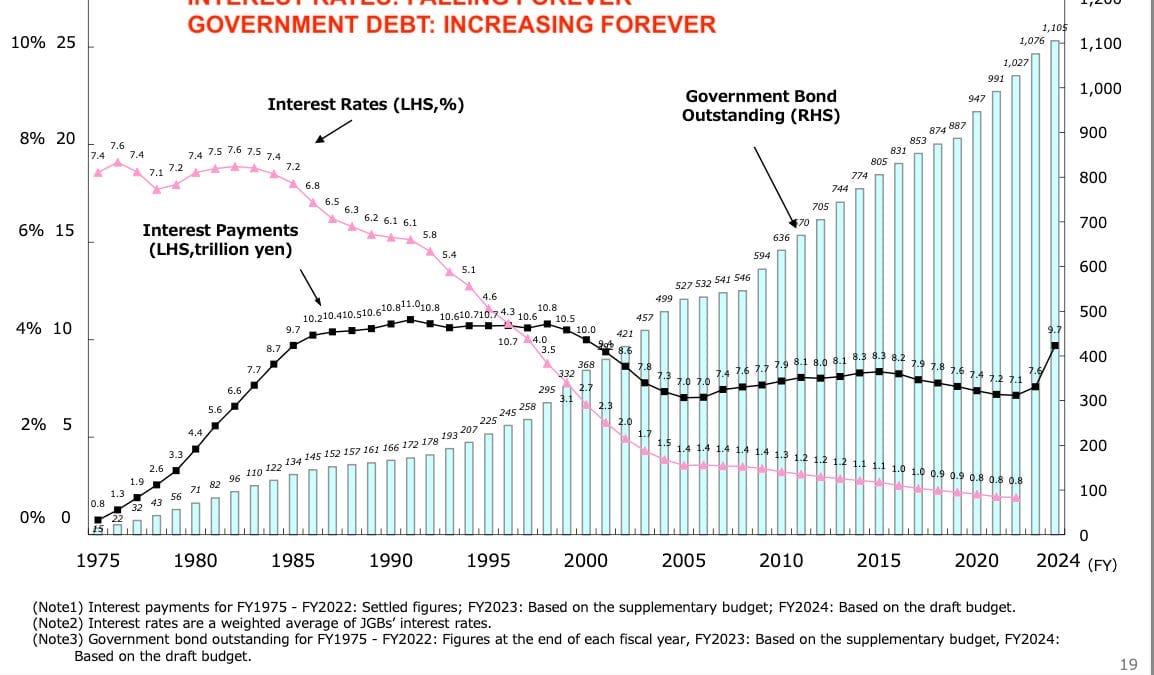

Policy Unwind

Japan was famous for its Near ZIRP (Zero-Interest Rate Policy) and its Yield Curve Control – but in October '22 I explained the time was right for the policy to reverse. Find it on X here.

THE CENTRAL BANK OF HARAKIRI.

— Philoinvestor (@philoinvestor) September 8, 2022

A thread🧵

"ritual suicide by disembowelment with a sword when disgraced or under sentence of death" pic.twitter.com/hhZOL58aYq

By December of that year, Kuroda's BOJ was forced to abandon the 25bps yield cap, expanding it to 50bps. Yields on the 10-Year doubled in a day.

By admitting defeat – the BOJ took the first step in the journey of retreating from direct intervention and in the path of unwinding its ultra-loose monetary policy.

To be fair, this ultra-loose wind down was met with the ascent of another policy: what I called managed-narrative float. That is, the BOJ would abandon YCC and let its yield curve float freely – but they would try to manage it by controlling the narrative.

That is, instead of directly intervening in markets, they would try to create the conditions they wanted by managing the narrative with words and posturing.

But markets see through all these tactics and always go where they will go. This is why it has been so hard trading the Yen for most.

I published this in June of 2024 — on the broader setup in Japanese macro.

I was right on the direction of Japan’s fiscal situation — but wrong on an easy linear down move by the Yen. The USD/JPY is only 1.5% higher than when I posted that piece, almost two years ago.

But I make this admission to bring another point across – that you can’t be married to your views in global macro.

Many have been burned trying to trade economics. Global macro trading is not economics. Moves in global macro instruments like commodities, FX and even the broader stock market are the shadows of economics (and a bunch of other things).

Don't get burned conflating the two. Learn to use technicals to structure your trades more intelligently.

My ability and willingness to stay flexible has made all the difference when trading the Yen, and macro instruments in general.

How I got lucky and bottom ticked the USD/JPY, mid-September 2024. $USD $JPY

— Philoinvestor (@philoinvestor) January 9, 2025

A small thread on this trade and my previous theses on the Yen. pic.twitter.com/0CooS1uZw2

Which brings us to the current setup.