Greater Fool Private Equity

The morphing landscape and its effect on PE sponsors.

“Private equity has absolutely no reason to exist. The private equity holder has all the upside and the banks all the downside.”

— Nassim Taleb

Nassim’s quote here isn’t entirely true though — is it? PE absolutely has a reason to exist: Since the GFC of 2008/2009, investors seemed to have had enough with the volatile nature of liquid (i.e. public) markets. Many were caught with their draws down (get it?), and that wasn’t consistent with their stated objectives and long-term investment vision — namely to generate above-average risk-adjusted returns over decades.

It seems the institutions of the world weren’t ready to deal with paradigm changes, shifting geopolitical climates, a turn from a value orientation towards growth investing etc.

Because of all this, and with the simple excuse (?) that “PE always overperforms all other asset classes” — they started moving more into PE investments.

And so, the rise and rise of Private Equity had begun.

Market Distortions

In the early days of PE, the predominant strategy was the LBO. A PE sponsor would agree on an acquisition target, raise a thin equity stack and borrow to the hilt to execute the Leveraged Buy Out (LBO). For me, the most iconic LBO was the one where KKR bought RJR Nabisco, you can watch the movie “Barbarians At The Gate” if you want to know more.

That deal basically marked the turn of PE from a nichey, exotic and non-mainstream asset class — to a generally accepted strategy. Note that KKR used 87% leverage for that deal, today leverage ratios on buyouts are running at half that!

In the olden days PE was the alternative — it was the deal that came out of nowhere to create value for the brave few that had allocated to the strategy. With good leverage, opportunistic price multiples and intelligent value creation it created massive value for its investors.

Nowadays PE is the market — and this is why it’s getting exponentially harder to gain an edge and overperform.

Too much money chasing too few returns…

First Principles of PE

In the early days of PE, leverage was easy, price multiples were low and competition was sparse. Now do you think any of that still holds? I think not.

With trillions more bidding up assets (basically, they are forced buyers) and borrowing costs moving up — PE has a problem.

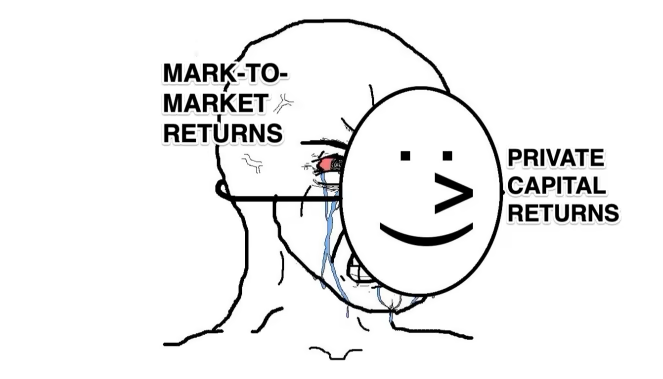

They still have the reputation that they overperform public equities, even if certain academics argue against that. They also still benefit from the fact that private markets don’t really mark-to-market in the same brutal way that public markets naturally do — allowing PE LPs to benefit from smoother and more “artificial” returns.

For now things are still OK, but the PE space relies on an infinite-life ever-increasing revolving fund of capital raising, capital returns (with a return!) and more capital raising.

With PE getting squeezed from all sides, do they have a trick up their sleeve?

Tailwinds are turning into Headwinds

Even the CIO of Singapore’s wealth fund (a prominent PE investor) agrees:

“Many of the things that were tailwinds for the private equity industry have come to an end... and I don't think they are coming back any time.”

Right now the space has ~$4 trln of dry powder ($1.2 trln in buyout alone) that they can deploy — but deploy where? Where will the growth come from? What levers will they pull to create the value that their LPs expect from them? And what enables PE to outperform other asset classes consistently over time?…

I won’t say Private Equity is a zero interest-rate phenomenon, because it isn’t only that. But to generate those returns that investors expect, one needs a certain type of interest-rate environment.

And even if one Sponsor offloads to another Sponsor, if the former Sponsor underwrote the asset at lower interest rates and the latter has to buy it with current interest rates — the numbers still don’t work.

Even if PE is not strictly a zero interest-rate phenomenon, rates are causing the market issues right now. For 2023, exits have dried up as IPOs, outright sales to strategic buyers and sponsor-to-sponsor sales have reduced significantly. This causes pressures to LP cash flows and forces Sponsors as a whole to extend (and pretend?).

This includes extending the life of a fund as well as launching continuation funds where the Sponsor sells the assets to himself (i.e. to a new fund launched by the same Sponsor) and extends the life of the investment even further.

A secondary transaction can also be used where a Sponsor sells an asset to another Sponsor. Secondary transactions come with their own prices — there is a market operating for those assets, meaning prices move wherever they may. Hint: You can’t always get your money back at par.

Sponsors even engage in the so called “NAV Financing”, which is basically a loan taken by the PE fund to give cash back to its LPs earlier than otherwise possible. Note: This increases leverage at the fund level.

All these are ways to keep the entry/exit machine going for the PE space in general, increase liquidity for LPs, and keep the whole space happy enough to keep reinvesting capital.

The revolving fund that we were talking about…

But the point is not to just get the LPs their money back, it’s to give them a return. So where did all those returns come from?

A study on buyout returns in the last decade concluded that 50% of returns came from revenue growth and the other 50% from multiple expansion. That means no returns came from margin expansion — the PE industry as a whole achieved no net performance boost in the reported margins of the companies they acquired!

If the multiple expansion for the market already happened, it means PE as a whole needs to keep finding and buying companies for lower multiples and sell them for higher multiples — not easy! Now targets know that PE is probably eyeing them, and they are pushing their ask prices higher and higher.

Furthermore, PE needs to continue to find companies that will benefit from revenue growth before they sell them to the next guy — but if the economy moves sideways for a few years, that will be practically impossible to achieve as a whole.

Let’s have a look into Real Estate PE vehicles and the Blackstone REIT…

Private Equity isn’t so Private Anymore (the rise of the Semi-Liquid)

Unlike a typical PE fund, the BREIT was designed as a perpetual fund that would allow wealthy investors to enter at whatever the fund’s net asset value is at the time. The BREIT was launched in 2017 and closed the year with $4.6bln in gross assets, by y/e 2022 it ran with >$120bln and a leverage ratio of 50%.

Note that Blackstone charges a 1.25% management fee on that AuM and a 12.5% carry above a 5% performance hurdle — the BREIT boasts an annualised performance to date of >10%.

The problem with the BREIT however is that it runs with an asset/liability mismatch — assets being the underlying RE and liabilities being the partner interests. You can’t sell the assets as fast as LPs can send redemption requests. Yes, Sponsors can raise gates but they can’t keep them up forever.1

Inter-connectedness & the Squeeeeeze

In late 2022 the BREIT ran into some problems. Turbulence in Asian markets caused some Asian investors to redeem their interest, forcing the BREIT to ultimately raise a gate disallowing LPs from redeeming their capital. 70% of redemptions came from Asia — it just so happened that those Asian investors needed their money.

They viewed the BREIT as a semi-liquid structure and so they asked to get their money back. What happens in even more extreme scenarios where say half of the investors need the money? That would turn said entity into a forced seller of its underlying assets — and when the market knows you are a forced seller (and a massive one at that) it will squeeze you.

Ultimately, the BREIT survived and redemptions stopped coming in. But is it too big for its own good? Can it grow and/or overperform from here? Have PE strategies in general overgrown the playground that they invest in?

If the PE space as a whole has had its best days then how will the publicly-listed PE sponsors perform going forward?

Next on Philoinvestor we will have a look into a bucket of publicly-listed Sponsors and what the current investment setup is.

Sincerely,

Philo 🦉

This comment on the FT illustrates in a comic way how the BREIT, by not being publicly traded, was able to report vastly different performance relative to its listed peers — giving rise to a private-to-public arbitrage that its LPs wanted to extract. ↩